Bonds: A Complete Guide on How to Invest in Bonds

April 11, 2025

12 min read

As the saying goes, don’t put all your eggs in one basket. Similarly, in finance, it is recommended that you invest your money across various assets, such as stocks and bonds. That way, when one type of investment does not perform well, you still have other sources of income.

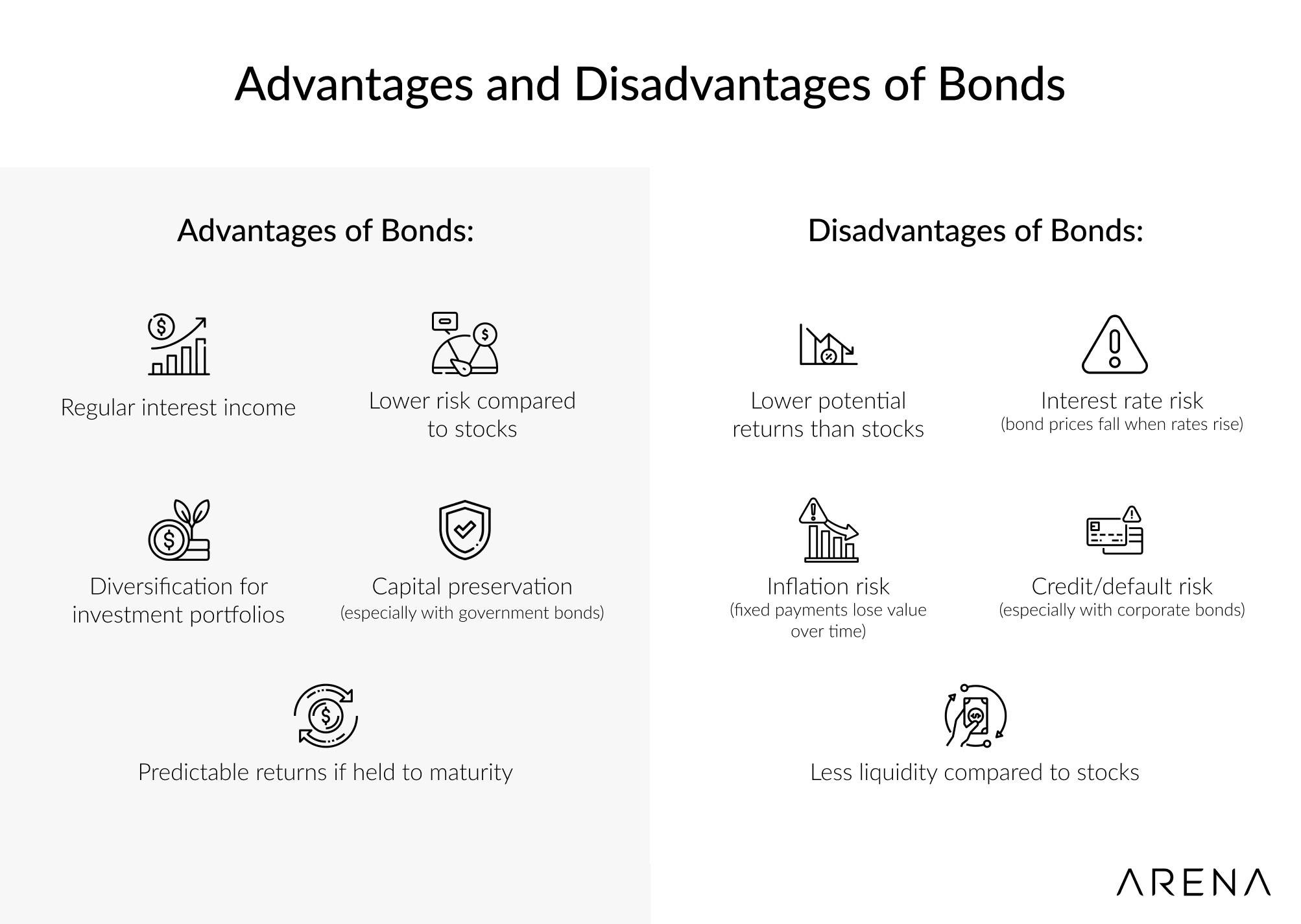

Bonds can play a vital role in a well-balanced investment portfolio, helping to mitigate risks. This is because stocks may offer higher returns, but they also tend to be more volatile. Bonds, on the other hand, typically provide steady income, making them a more reliable option during market fluctuations. By including both stocks and bonds in your portfolio, you maximise growth potential and gain financial security, protecting your investments over time.

Whether you’re a cautious investor seeking predictable returns or a seasoned one looking to diversify assets, understanding how bonds work is essential. In this guide, we’ll explore what bonds are, how they generate returns, the different types available, and why they are a smart addition to many investment strategies.

Key Takeaways:

Bonds are fixed-income instruments since issuers pay investors a fixed interest rate, known as the coupon.

Bonds have a set maturity date, which is when the issuer must repay the full amount borrowed, or risk defaulting.

Bond prices have an inverse relationship with interest rates: when rates increase, bond prices decrease, and vice versa.

What is a Bond

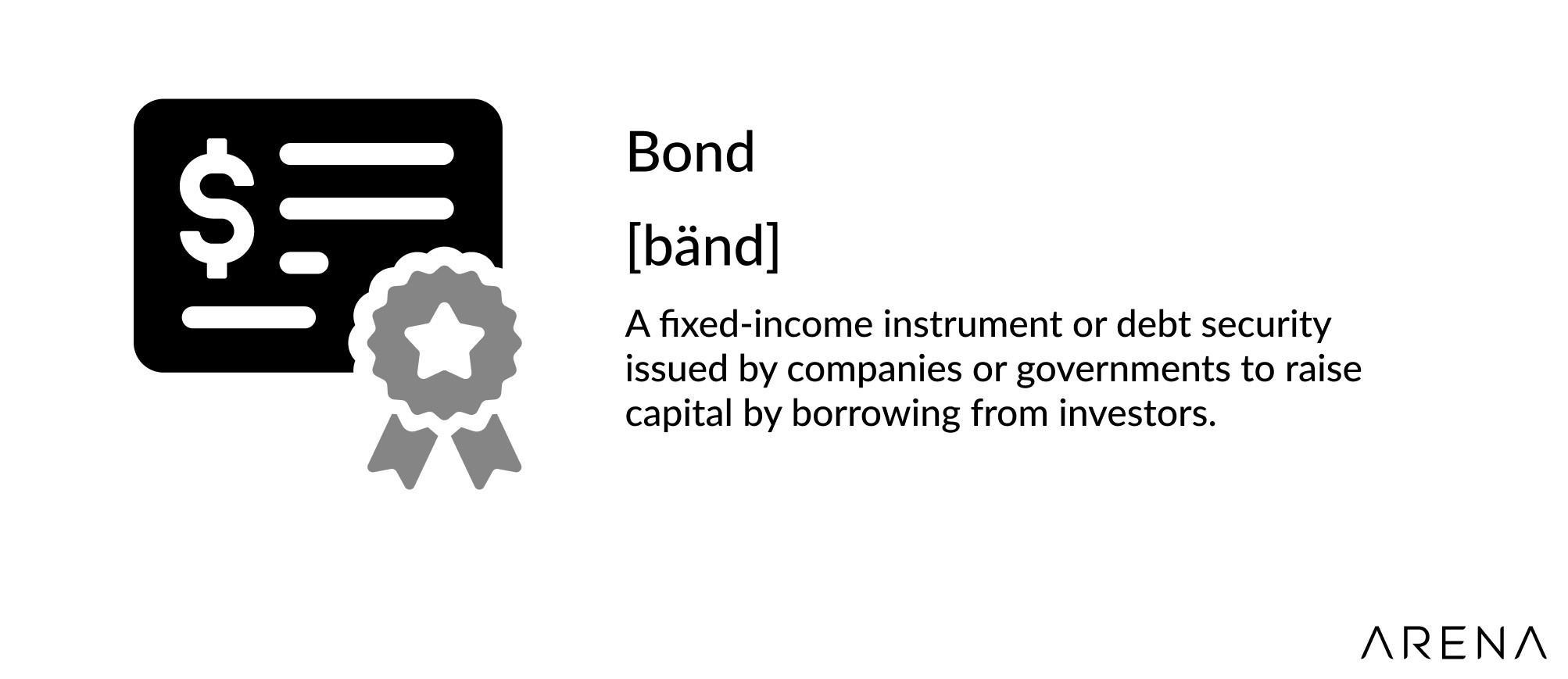

A bond is a fixed-income investment option where individuals lend money to a company or government entity at a certain interest rate and for a set duration. The borrower repays the individual the original face value at a specified time (maturity), plus the interest rate spread over the bond's duration.

Generally, bonds are issued by companies, states, municipalities, and sovereign governments when they need capital to finance projects and operations.

Investors who purchase bonds can then be referred to as bondholders or creditors of the issuer. For instance, investing in corporate bonds means you are lending money to a company.

A well-structured bond outlines key details, including the maturity date when the face value will be repaid to the bondholder. It also provides a clear breakdown of the terms for interest payments, whether fixed or variable, that the issuer is required to make.

Characteristics of Bonds

Par or Face Value

The par or face value of a bond is the principal amount the issuer pays the bondholder. It is also the amount on which interest payments (coupon) are calculated.

Issue Price

The price at which the bond was originally sold to investors when it was first offered by the issuer.

Coupon

The coupon is the fixed annual interest rate that the issuer agrees to pay the bondholder until the bond matures. It is expressed as a percentage of the bond’s face value. For example, a $1000 investment in AIX Bonds with a 12% annual yield or a 3% quarterly coupon rate for a 60-month duration will amount to $120 in interest per year.

Coupon Dates

The specified dates on which the bond issuer will make interest payments to the bondholders.

Maturity Date

The specified date at which the bond will mature, and the bond issuer will pay the principal or face value of the bond to the bondholder.

How Bonds Work

When you purchase bonds, you basically assume the role of a creditor or lender–letting businesses or governments borrow your money. In return, you gain a steady income from regular interest payments.

To further explain how bonds work, let’s say you invest $10,000 in AIX bonds, which are usually sold at $1000 each. These bonds have a 12% annual yield or a 3% quarterly coupon rate spread across a duration of 60 months, plus a 100% payback value.

Face Value = $10,000

Issue Price = $ 1,000

Interest = 12% annually or 3% quarterly of $10,000

Maturity = 60 months (5 years)

Explanation:

AIX, as the bond issuer, promises to pay you $300 every 3 months, allowing you to earn a total of $1,200 per year until your bond matures. After 60 months or upon maturity, they will also return your $10,000 investment in full.

The coupon and maturity of the bond are crucial in evaluating the returns and risks an investor can expect from bonds.

Ideally, bond issuers set the coupon based on the current market interest rates to remain competitive. The coupon gives investors an idea of how much interest they could earn on top of the money they are lending, making the bond more appealing compared to others.

Maturity or the duration of the bond is another consideration because certain situations over an extended period of time may affect the issuer’s ability to repay investors. In the case of long-term bonds, the bond issuer usually offers higher interest rates to compensate for the greater risk of default–not being repaid.

Bond Categories

Bonds sold in trade markets fall under three primary categories. However, you may also see foreign bonds issued by global corporations and governments on some platforms.

Government Bonds

Government bonds are issued by treasuries and are classified based on their maturity or duration:

Bills - mature within or after 1 year from the issuing date.

Notes - matures between 2 and 10 years from the issuing date.

Bonds - maturity ranges from 10 to 30 years, with fixed interest rates.

The government bond sector is a broad category that includes sovereign debt, which is issued and generally backed by a central authority. Europe, Japan, and the U.S. government bond markets have both historically and recently been the biggest issuers.

Some governments also issue sovereign bonds that hedge against inflation. These are called inflation-linked bonds or, in the U.S., Treasury Inflation-Protected Securities (TIPS). This type of government bond regularly adjusts the interest and/or principal to reflect changes in the inflation rate.

In addition to sovereign bonds, the government bond sector includes subcomponents, such as:

a. Agency and “Quasi-Government” Bonds

These are bonds issued by agencies or government-related organizations to finance public projects or initiatives, including those that promote affordable housing and support small and medium-sized enterprises (SMEs). However, some agency bonds are guaranteed by the central government, while others are not.

b. Local Government or Municipal Bonds

Local governments, divided by provinces, cities, or states, issue bonds to fund their projects, such as building bridges, renovating schools, and other general purposes.

Corporate Bonds

Next to the government sector, corporate bonds have been the largest segment in the market. They are issued by companies to finance debt for expanding operations or funding new ventures.

Businesses often opt for corporate bonds instead of seeking bank loans, as they offer more favourable terms and lower interest rates. Corporate bonds can be classified as:

Investment Grade Bonds

Investment-grade bonds are generally considered low risk by credit rating agencies. These bonds are issued by financially stable companies that are likely to repay their debt on time.

Speculative-Grade Bonds

Also known as high-yield or junk bonds, these are issued by newer companies that operate in volatile industries or those with weak financials. These companies tend to have lower credit ratings, which means their speculative-grade bonds carry a higher risk of default.

Corporate bonds typically offer higher coupon rates to compensate for the increased risk involved. If a company’s financial situation gets worse, its credit rating can be downgraded, making its bonds riskier. On the other hand, if the company’s finances improve, its rating can be upgraded, making its bonds more attractive to investors.

Emerging Bonds

Sovereign and corporate bonds issued by developing countries are called emerging market (EM) bonds. They are issued in major global currencies, such as the U.S. dollar, the euro, and the British pound.

Since emerging bonds come from various countries, each with its own growth potential, they help investors diversify their investment portfolio and balance their risk and return profile.

Quick Trivia:

Did you know that Nasdaq Dubai welcomed the Middle East’s first $100 million Blue Bond listing by DP World?

It is a type of sustainability bond that is specifically used to finance projects that protect and preserve water-related ecosystems. Examples of “blue” initiatives include coastal restoration, pollution reduction, marine conservation, and the regulation of ethical fishing.

Understanding Duration in Bond

In finance or investment, the duration of a bond can be viewed from two perspectives.

Macaulay Duration

Refers to the average time taken for a bond’s cash flows (coupon + principal) to be paid. It is often expressed in years, which helps investors understand the timing of payments.

Modified Duration

Measures how much a bond’s price will change if interest rates go up or down by 1%. It helps investors understand the bond’s sensitivity to interest rate changes—the higher the modified duration, the more the price will fluctuate when rates change.

The duration of a bond can be a good basis for investors to estimate how bond prices will change in response to fluctuations in interest rates. Generally, bonds with longer maturities and lower coupons are more sensitive to interest rate changes.

Yield-to-Maturity (YTM)

The Yield-to-Maturity (YTM) is a metric that estimates the total return an investor can expect if they hold the bond until maturity, assuming all payments are made as scheduled. Although YTM is typically associated with long-term bonds, it is expressed as an annual percentage rate.

YTM helps investors compare bonds with different interest rates and maturity dates to see which one is more attractive. Below is the formula to calculate YTM and the values to look for.

Where:

C = Interest/coupon payment

FV = Face value of the bond

PV = Present value/price of the bond

t = Years it takes the bond to reach maturity

What Determines a Bond's Coupon Rate?

Credit quality and time to maturity influence a bond’s coupon rate. If the bond issuer has a low credit rating, the chances of default are greater, contributing to a higher coupon rate to compensate investors taking on more risk. Similarly, a bond with a longer maturity also offers a higher coupon rate. This helps offset the risks associated with interest rate fluctuations and inflation, to which bondholders can be exposed over an extended period.

How Are Bonds Rated?

Credit rating agencies such as Standard & Poor's, Fitch Ratings, and Moody's assign ratings to both companies and the bonds they issue. These ratings assess the creditworthiness of the issuer and the likelihood of bond repayment.

Key Elements That Determine Bond Value in the Secondary Market

Once bonds are issued, they can also be bought and sold in the secondary market. Some bonds are publicly traded through exchanges. Many also opt to trade over-the-counter between large brokers or dealers, who do so on behalf of their clients or for their own accounts.

A bond’s price and yield determine its value in the secondary market. A bond has a face value at which it can be bought and sold, and its yield is the annual return the investor can expect if the bond is held to maturity. Yield is determined based on the bond’s purchase price and its coupon (interest rate).

The price of a bond moves opposite to its yield—when the yield goes up, the price goes down, and when the yield goes down, the price goes up. The price of a bond reflects the value of the interest payments it offers to investors.

When interest rates drop, especially for government bonds, older bonds become more valuable because they were issued with higher interest rates. As a result, these bonds can be sold at a premium (above par value) in the market. On the other hand, if interest rates rise, older bonds with lower interest rates become less attractive and are sold at a discount (below face value).

Bond Prices vs Interest Rates: An Example

The issuer of a fixed-rate bond agrees to pay a coupon based on its face value. For example, a $1,000 par and a 10% annual coupon will pay the bondholder $100 per year.

If the current interest rate is also 10% at the time the bond is issued, there are no significant differences in choosing between a corporate or government bond. However, if the interest rate drops to 5%, the investor can only receive $50 from the government bond, but can still receive $100 from the older corporate bonds, making it more attractive. This makes investors bid higher for the older bonds until they trade at a premium price, which equals the current interest rate.

In this example, the older bonds will be traded at $2,000, so that the coupon represents a 5% yield ($100 interest ÷ $2,000 price = 5% yield - matching the new market rate).

Similarly, if interest rates soared to 15%, investors could make $150 from government bonds, making them even more attractive than the $100 from corporate bonds. In this case, the bond will be sold until it reaches a discount price that equals the yields, which is $666.67 ($100 annual interest ÷ $666.67 price = 15% yield or the new prevailing market interest rate)

Bond Variations

Bonds can also be classified based on the following criteria:

The rate or type of coupon payments

Whether or not they are redeemable before the maturity date, typically at a premium.

Additional features attached to the bond

Zero-Coupon Bonds (Z-bonds)

A zero-coupon bond doesn’t pay interest. Instead, it’s sold at a lower price than its face value, and you get the full amount back when it matures. The difference between what you pay and what you get back is your profit.

Convertible Bonds

Convertible bonds are debt instruments that give the bondholder the option to convert their bonds into a predetermined number of shares or equity in the issuing company at a specified time. This conversion is typically influenced by conditions such as the stock price reaching a certain level.

Callable Bonds

A callable bond can be called back by the company or issuer before it reaches maturity. This type of bond can be riskier for the investor as the probability of the bonds being redeemed when their value is rising is higher.

Puttable Bonds

Puttable bonds give bondholders the option to put or sell the bonds back to the issuing company before they reach maturity. They’re ideal for investors who are concerned that a bond may decrease in value if interest rates rise, and want to recover their principal before the bond's value falls. Puttable bonds are usually traded at a higher value than regular bonds with the same credit rating, maturity, and interest rate.

Building Financial Stability By Investing in Bonds

Bonds offer a solid foundation for investors seeking financial stability, steady income, and asset diversification. They are a lower-risk alternative compared to other types of investments, such as stocks. Bonds also provide predictable returns and help cushion your portfolio against market volatility. Understanding how to invest in bonds allows you to make informed decisions that align with your long-term investment goals.

ARENA Capital is a family-run consultancy and venture capital group. This blog is for informational purposes only and should not be considered financial advice. We recommend you consult a licensed financial advisor before making any investment decisions. We will not be liable for any actions taken based on this content.